Introduction

Every financial decision a business makes leaves a trail. That trail lives inside a ledger account, quietly recording what comes in, what goes out, and where the money actually stands. Without it, accounting would be guesswork instead of precision.

If you’ve ever wondered how companies know exactly how much they owe, earn, or own at any given moment, the answer almost always starts with a ledger account. It’s the backbone of accounting, whether you’re running a small shop, studying commerce, or managing corporate finances.

In reality, many people hear the term but never fully understand how it works or why it matters so much. Let’s break it down in a clear, human way—no jargon overload, no robotic explanations—just practical clarity.

Table of Contents

Table of Contents

What Is a Ledger Account

Why a Ledger Account Matters in Accounting

Structure of a Ledger Account

Types of Ledger Account

How Ledger Accounts Work in Real Life

Journal vs Ledger Account

Rules of Debit and Credit in Ledger Account

Ledger Account Examples (With Tables)

Common Mistakes in Maintaining Ledger Accounts

Ledger Account in Modern Accounting Software

Personal Background and Financial Insight (Accounting Profession)

FAQs

Conclusion

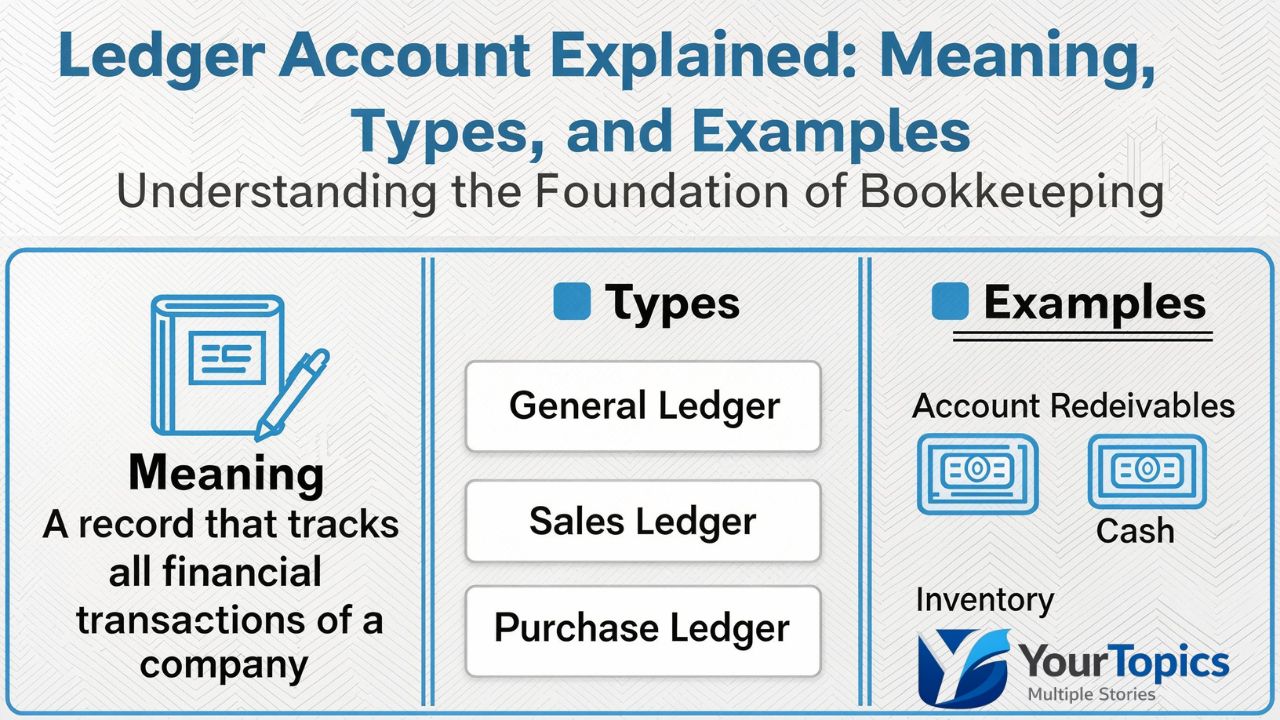

What Is a Ledger Account

A ledger account is a detailed record that summarizes all financial transactions related to a specific item, such as cash, sales, purchases, assets, or liabilities. Each account shows debits on one side and credits on the other, allowing accountants to track balances accurately.

In simple words, think of it as a dedicated folder for one financial item. Every time money affects that item, the transaction is posted into its ledger account.

A ledger account doesn’t exist on its own. It is created after transactions are first recorded in a journal and then classified into individual accounts for clarity and control.

Why a Ledger Account Matters in Accounting

Without ledger accounts, financial statements would collapse under confusion. Journals record transactions chronologically, but they don’t show balances. Ledger accounts solve that problem.

Here’s why they matter so much:

- They show the current balance of each account

- They help detect errors and discrepancies

- They form the base of trial balance preparation

- They support accurate profit and loss calculations

- They ensure accountability and transparency

On the other hand, poorly maintained ledger accounts can lead to incorrect reports, tax issues, and even legal trouble. That’s why accountants treat them with extreme care.

Structure of a Ledger Account

A typical ledger account follows a “T-format,” although modern software displays it digitally.

Basic Parts of a Ledger Account

- Account Title (e.g., Cash Account)

- Debit (Dr) Side

- Credit (Cr) Side

- Date of transaction

- Particulars (description)

- Amount

- Balance carried forward

The left side always represents debit entries, while the right side represents credit entries. This structure keeps records clean and balanced.

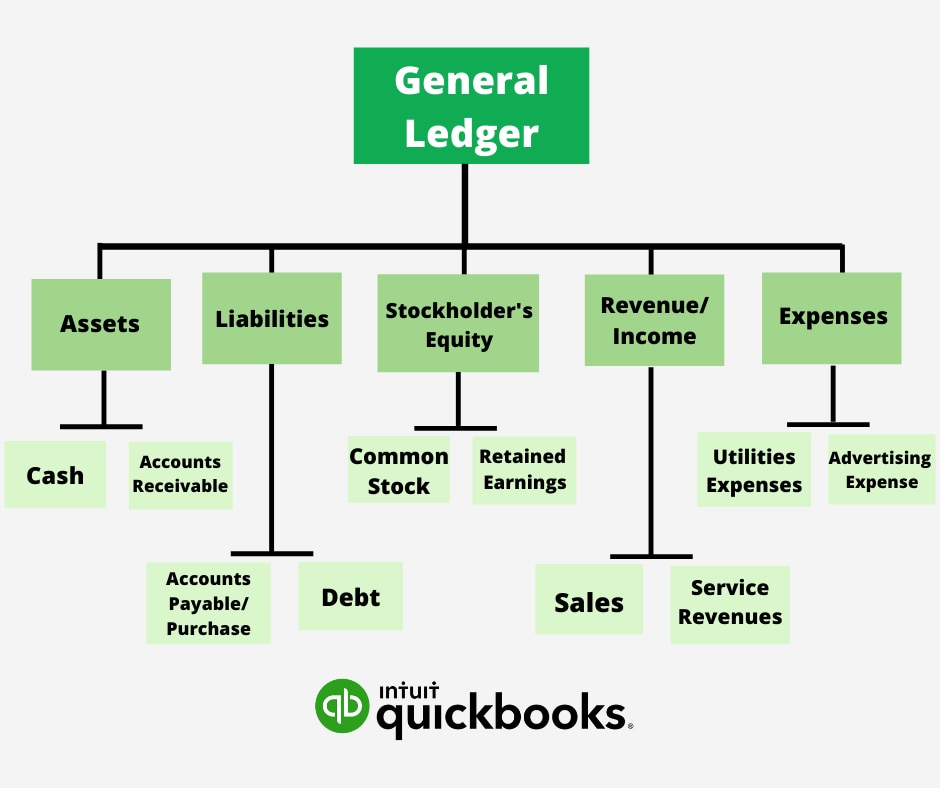

Types of Ledger Account

Ledger accounts are classified based on the nature of transactions they record.

Personal Ledger Account

These relate to individuals, firms, companies, or institutions.

Examples:

- Customer accounts

- Supplier accounts

- Bank accounts

Rule: Debit the receiver, credit the giver.

Real Ledger Account

These relate to assets and properties.

Examples:

- Cash account

- Furniture account

- Machinery account

Rule: Debit what comes in, credit what goes out.

Nominal Ledger Account

These relate to expenses, incomes, gains, and losses.

Examples:

- Salary account

- Rent account

- Commission received

Rule: Debit expenses and losses, credit incomes and gains.

Each ledger account fits into one of these categories, which makes posting systematic and logical.

How Ledger Accounts Work in Real Life

Imagine a small business purchasing office furniture for cash.

Step one: The transaction is recorded in the journal.

Step two: It is posted to:

- Furniture account (debit)

- Cash account (credit)

Over time, these entries accumulate. At any moment, the business owner can open the ledger account and see exactly how much furniture value exists or how much cash remains.

In reality, this system prevents financial blind spots. You’re not guessing—you’re seeing.

Journal vs Ledger Account

Many beginners confuse journals and ledgers, but their roles are different.

| Feature | Journal | Ledger Account |

|---|---|---|

| Purpose | Record transactions | Classify transactions |

| Order | Chronological | Account-wise |

| Detail | Brief | Detailed |

| Balance shown | No | Yes |

A ledger account turns raw transaction data into usable financial insight.

Rules of Debit and Credit in Ledger Account

Debit and credit aren’t about “good” or “bad.” They’re about position and impact.

Basic Debit-Credit Rules

- Assets increase → Debit

- Assets decrease → Credit

- Liabilities increase → Credit

- Expenses increase → Debit

- Income increases → Credit

Understanding these rules makes ledger posting almost automatic with practice.

Ledger Account Examples (With Tables)

Cash Ledger Account Example

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| Jan 1 | Capital Introduced | 50,000 | |

| Jan 5 | Furniture Purchased | 10,000 | |

| Jan 31 | Balance c/d | 40,000 |

This ledger account shows how cash moved during the period and what balance remains.

Sales Ledger Account Example

| Date | Particulars | Debit | Credit |

|---|---|---|---|

| Jan 10 | Credit Sales | 15,000 | |

| Jan 31 | Balance c/d | 15,000 |

Only relevant transactions appear in each ledger account, keeping records clean and focused.

Common Mistakes in Maintaining Ledger Accounts

Even experienced businesses make errors.

Common issues include:

- Posting to the wrong ledger account

- Ignoring narration details

- Mixing personal and business accounts

- Skipping balance verification

- Incorrect debit-credit application

However, regular reconciliation and trial balances catch most mistakes early.

Ledger Account in Modern Accounting Software

Today, software like QuickBooks, Xero, and SAP automates ledger posting. But the logic remains identical.

Behind every click:

- Transactions still post into ledger accounts

- Debit and credit rules still apply

- Balances still drive reports

Understanding the manual concept of a ledger account makes software usage far more powerful and less error-prone.

Personal Background and Financial Insight (Accounting Profession)

Most professional accountants begin their journey mastering ledger accounts. It’s often the first real “aha” moment in accounting education.

Over time, ledger expertise leads to roles in:

- Financial analysis

- Auditing

- Corporate finance

- Tax advisory

Financially, qualified accountants often enjoy stable income growth. Entry-level roles may start modestly, but experienced professionals managing complex ledger systems command strong compensation, especially in multinational firms.

Ledger mastery isn’t glamorous—but it’s lucrative.

FAQs

Frequently Asked Questions

What is a ledger account in simple words?

A ledger account is a record that shows all transactions related to one item, such as cash or sales, in one place.

Why is a ledger account important?

It helps track balances, prepare financial statements, and ensure accuracy in accounting records.

Is a ledger account debit or credit?

It contains both debit and credit sides. The balance depends on transaction types.

How many types of ledger account exist?

There are three main types: personal, real, and nominal.

Can a ledger account show losses?

Yes, nominal ledger accounts record expenses and losses.

Is ledger account used in small businesses?

Absolutely. Even the smallest businesses rely on ledger accounts, often through accounting software.

What comes first, journal or ledger?

Journal entries are recorded first, then posted into ledger accounts.

Is ledger account still relevant with software?

Yes. Software automates it, but the ledger account remains the foundation.

Conclusion

Accounting may evolve, software may change, but the ledger account remains timeless. It brings order to financial chaos, clarity to decision-making, and confidence to business operations.

Whether you’re learning accounting, running a business, or managing finances professionally, understanding ledger accounts isn’t optional—it’s essential. Once you truly grasp how they work, the entire accounting system starts to make sense, almost effortlessly.

And that’s the real power of a ledger account.